Build-to-rent (BTR), a fairly new concept in our property landscape, has been brought up as a possible method to increase housing supply and alleviate housing shortages. So, what does it involve and what is its current state in Australia?

To understand it’s potential impact on the rental market, we will explore what BTR is, the advantages it can bring, the state of the sector overseas, and how the Australian market differs.

In Australia, build-to-sell is the most common model of home construction, where developers construct homes to sell individually. For BTR, developers or investors own and rent out whole complexes after their construction.

The differences in the objective of these models results in BTR developments having unique features that are advantageous to renters and developers.

Developers of BTR properties are able to forgo public marketing and pre-sale phases associated with build-to-sell. As construction is not as impacted by sentiment and financing from individual investors, this can enable development that otherwise wouldn’t be possible.

Maintaining ownership of the building after construction also allows them to have a clearer picture of the end users and construct properties to meet their needs. This can result in higher quality developments which attract higher rents.

For renters, BTR homes often offer longer leases than the typical 12 months. In addition, the property management is closely associated with the building owner and has incentives to repair and maintain properties promptly.

As the model allows developers to build a large number of homes at scale, it can also play an important role in improving housing supply.

BTR is prominent in countries like the US and gaining momentum in the UK.

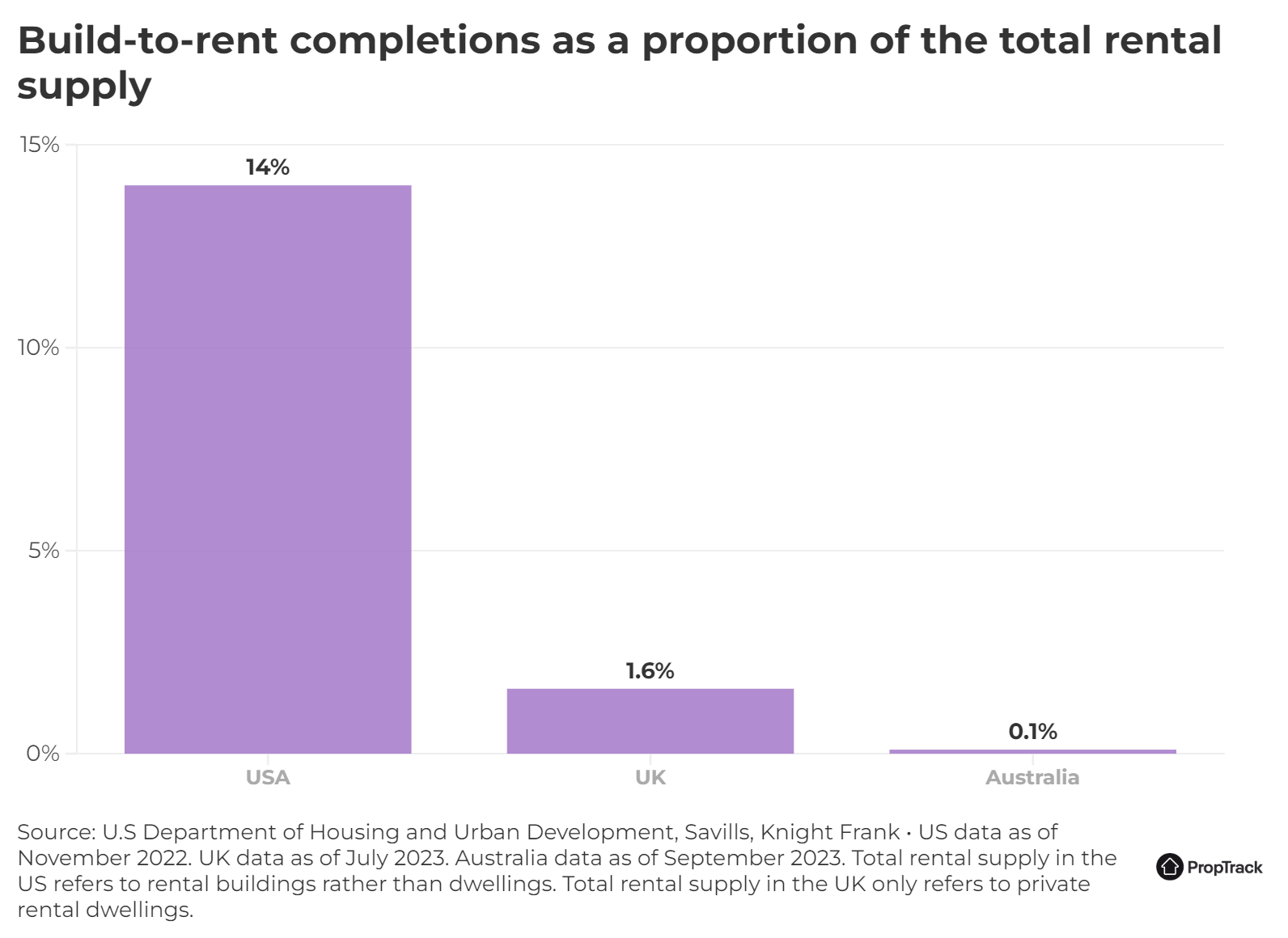

Build-to-rent makes up just 0.6% in Australia[1], 2.8% of rental properties in the UK[2] and 14% in the US[3].

In recent years, the number of BTR* developments in the US has increased substantially following the downward trend in vacancy rates. Vacancies fell to 5.7% in 2020, their lowest level since 1984[4]. To address the shortages in rental supply, starts in BTR projects hit a three-decade high in late 2021 with the commencement of 466,000 units while another 600,000 were under construction[5].

In the UK, BTR has been supported as a method to address the rental crisis. Institutional investment has grown from £2.5b in 2011 to just under £4.5b in 2022. As of Q2 this year, there are 253,400 homes either completed, or in the pipeline[2].

US and UK governments view BTR as an important source of new housing supply. This is evident in the policies, laws and concessions created to promote the growth of this sector.

In the US, loans for BTR are backed by government-chartered agencies Fannie Mae and Freddie Mac who purchase mortgages from lenders, pool them into mortgage-backed securities and sell them to investors on a secondary market. The payment on securities is guaranteed by these agencies. This minimises the risk of default for developers and institutional investors and encourages them to build or buy more developments[6].

In the UK, a BTR fund was introduced in 2013 – providing £1.1b in debt financing for developers who constructed purpose-built rentals. This was designed with the intention of driving investment into the sector and fast-tracking the building of new rental homes[7].

Compared to the US and UK, Australia’s BTR sector is relatively new.

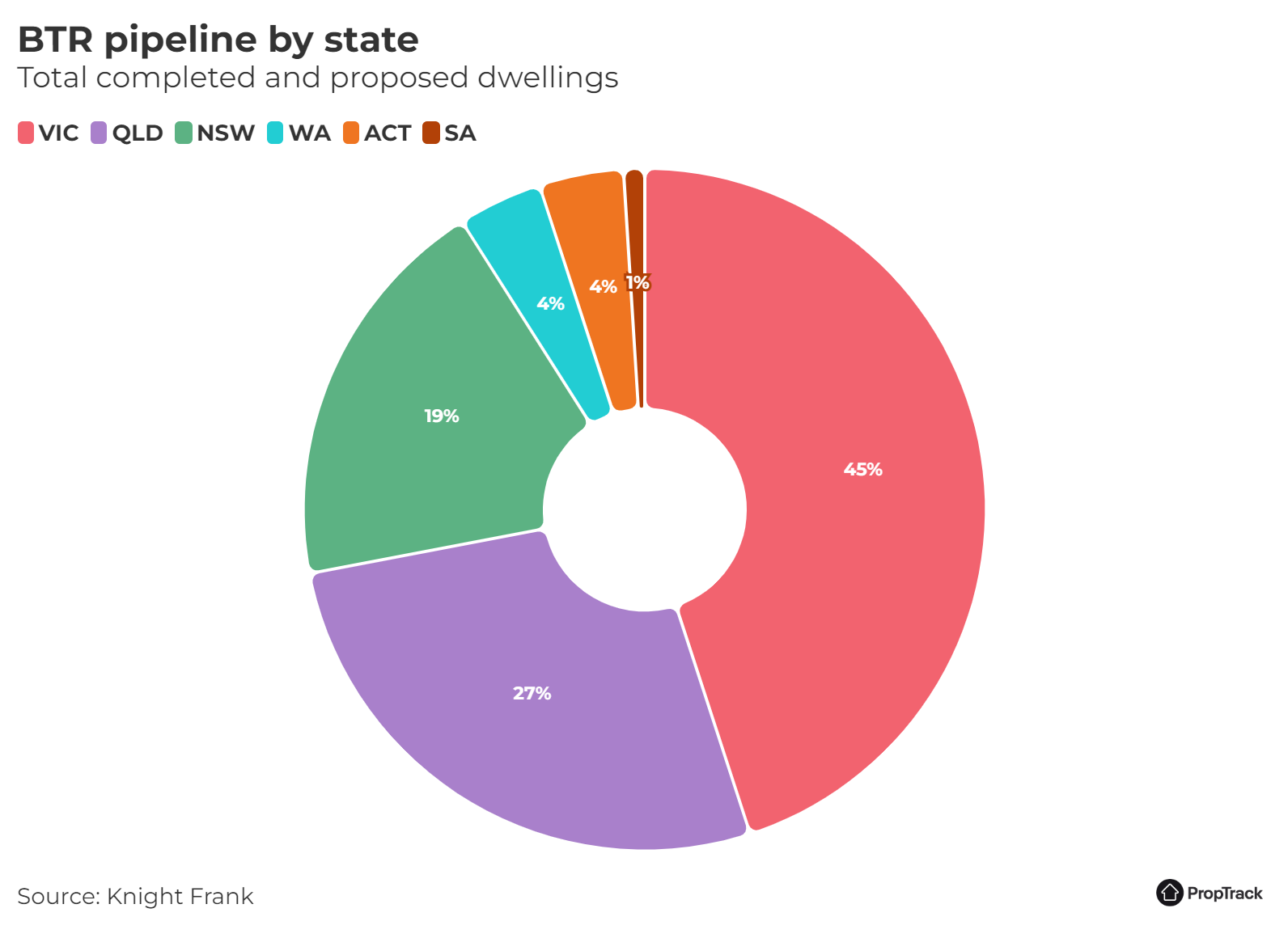

Currently there are just 4,340 BTR dwellings nationally, with another 8,914 under construction[8]. A large proportion of supply is in Victoria (45%) with 27% in Queensland and 19% for New South Wales[1].

The small size of the market can be attributed to unfavourable tax treatment which discouraged institutional investment.

Previously, managed trusts had to pay 30% tax on BTR projects with the government grouping it as a separate asset class. This made it less attractive compared to assets like commercial property which was taxed at 15%.

Land taxes on BTR were also calculated on the full value of the development, which inflated costs associated with building multi-dwelling complexes.

However, recent policy changes and tax incentives were proposed and instated by national and state governments to stimulate growth in the sector.

The tax rate for managed investment trusts is set to drop from 30% to 15% on 1 July 2024 and most states with a stake in BTR have provided a 50% land tax discount to encourage construction.

Although BTR is still a nascent industry in Australia, the growth and size of the BTR market in other countries like the US and UK provide evidence of the potential for it to improve rental supply.

Tax incentives introduced by the government in the past six months show that they support the expansion of the sector in the long run.

While BTR is unlikely to improve conditions in the market in the near term, it has the potential to provide a substantial number of homes for the future, especially by facilitating increased investment from institutional and overseas investors.

[1] BTR sector in Australia forecast to see 55,000 dedicated units by 2030

[2] UK Build to Rent Market Update – Q2 2023

[3] HUD and Census Bureau release findings of 2021 rental housing finance survey

[4] The Rental Housing Crisis Is a Supply Problem That Needs Supply Solutions

[5] America’s rental housing 2022

[6] How Fannie Mae and Freddie Mac work

[7] Funding package to deliver thousands of new homes

[8] Australia’s build to rent sector

*In the US, build-to-rent is often known as the "multi-family" sector.