Home prices in regional areas have grown slower than in the capitals this year, but the latest data shows the regions are starting to catch up.

The regions outperformed during the pandemic boom, and prices held up better than in the capital cities for much of 2022.

But capital city prices took the lead this year, rising 5.95% from a low in December 2022, compared with 2.43% growth in the regions.

Despite values stabilising in recent months, the regional recovery has lagged metro areas.

One reason why prices in the regions haven’t continued their stretch of outperformance has been the increase in choice for buyers. Stock for sale has increased, and paired with easing demand, price growth has softened with regional markets lagging their capital city counterparts.

The pandemic years drove record demand for regional property which resulted in an intensely competitive market. Increased supply has aided in cooling these competitive conditions.

Difficult purchasing conditions have eased for regional buyers in NSW, Victoria, Tasmania and NT, with the number of properties listed for sale normalising after some very tough years. However, the supply of homes for sale remains tight in regional Queensland, SA and WA.

Total listings in regional NSW rose 4.4% over September to reach the highest level in close to three years, while total listings in regional Victoria and Tasmania were 37.6% and 30.7% higher year-on-year respectively in September.

People are still moving from the capital cities to regional areas, though the pace they are doing so has eased from the above-average levels seen through the pandemic period. At the same time, more people are moving from regional areas to cities than was occurring during the pandemic period.

Despite lagging capital city markets, the pace of growth in regional markets has increased in recent months. In October, regional prices rose 0.32%, completely reversing falls in 2022 and early 2023 to set a record high.

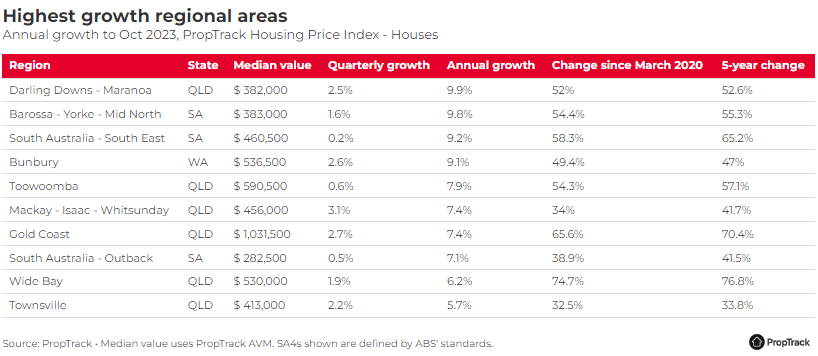

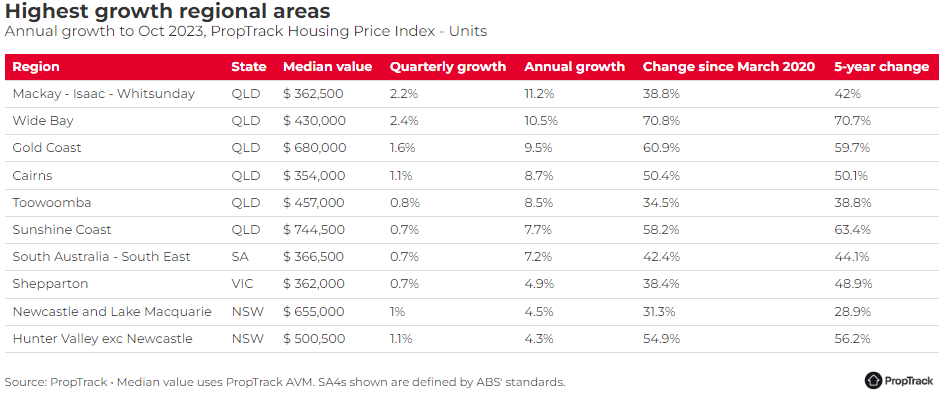

The strongest growth has been in more affordable regions in Queensland, South Australia and Western Australia.

These better performing regional markets continue to benefit from pandemic-induced preference shifts, relative affordability advantages, agricultural and mining exposure, and population flows. These are also regions where the supply of stock for sale remains more limited, with stronger competition bolstering prices.

Demand for more affordable homes following substantial interest rate rises has provided support and these markets have been the strongest performing regional areas over the past year.

Unit values in southeast Queensland have performed particularly well, alongside commutable NSW regions, likely reflecting affordability constraints. Many jobs have remained flexible and capital city housing is much less affordable relative to regional counterparts.

Affordability advantages and population flows are also supporting prices in regional SA and WA, alongside less stock for sale and in some pockets, mining and agriculture exposure.

Regional Victoria and Tasmania are home to the worst performing regions over the past year.

Despite some regional markets recording strong growth, higher interest rates and slowing demand in the regions as population flows ease have weighed on values this year, with regional markets being much slower to join the 2023 price upturn.

After holding interest rates steady for four consecutive months, the Reserve Bank resumed its tightening cycle in November and lifted the cash rate to 4.35%.

Reduced borrowing capacities, increasing mortgage servicing costs and normalising migratory patterns remain a headwind for growth.

While the outlook for interest rates remains uncertain, some expect rates will stay high for some time, while others expect interest rates will be cut at some point in the second half of 2024.

The Reserve Bank has modestly increased its long-term inflation forecasts, indicating interest rates may remain higher for longer with possible further increases.

Unless inflation moves lower more quickly than expected in the months ahead it’s unlikely interest rates will be moving lower any time soon.

With affordability remaining stretched and worsening, the continued rise in capital city home values may price out a growing number of buyers, buoying well-located regional areas in 2024.